Inspired

Performance

Overview

Triveni Turbine Limited is firmly dedicated to achieving sustainable growth and creating value in the long-term. We believe that in order to create shareholder value, we must address other stakeholders as well. In line with the above philosophy, our Company continuously strives for excellence through adoption of best governance and disclosure practices. Our Company recognises that good governance is a continuous exercise and thus reiterates our commitment to pursue highest standard of Corporate Governance in the overall interest of our stakeholders. Our Company also promotes a high level of transparency and accountability in internal and business conduct.

Investor Kit

Quarter-Wise

Performance FY26

Revenue from Operations

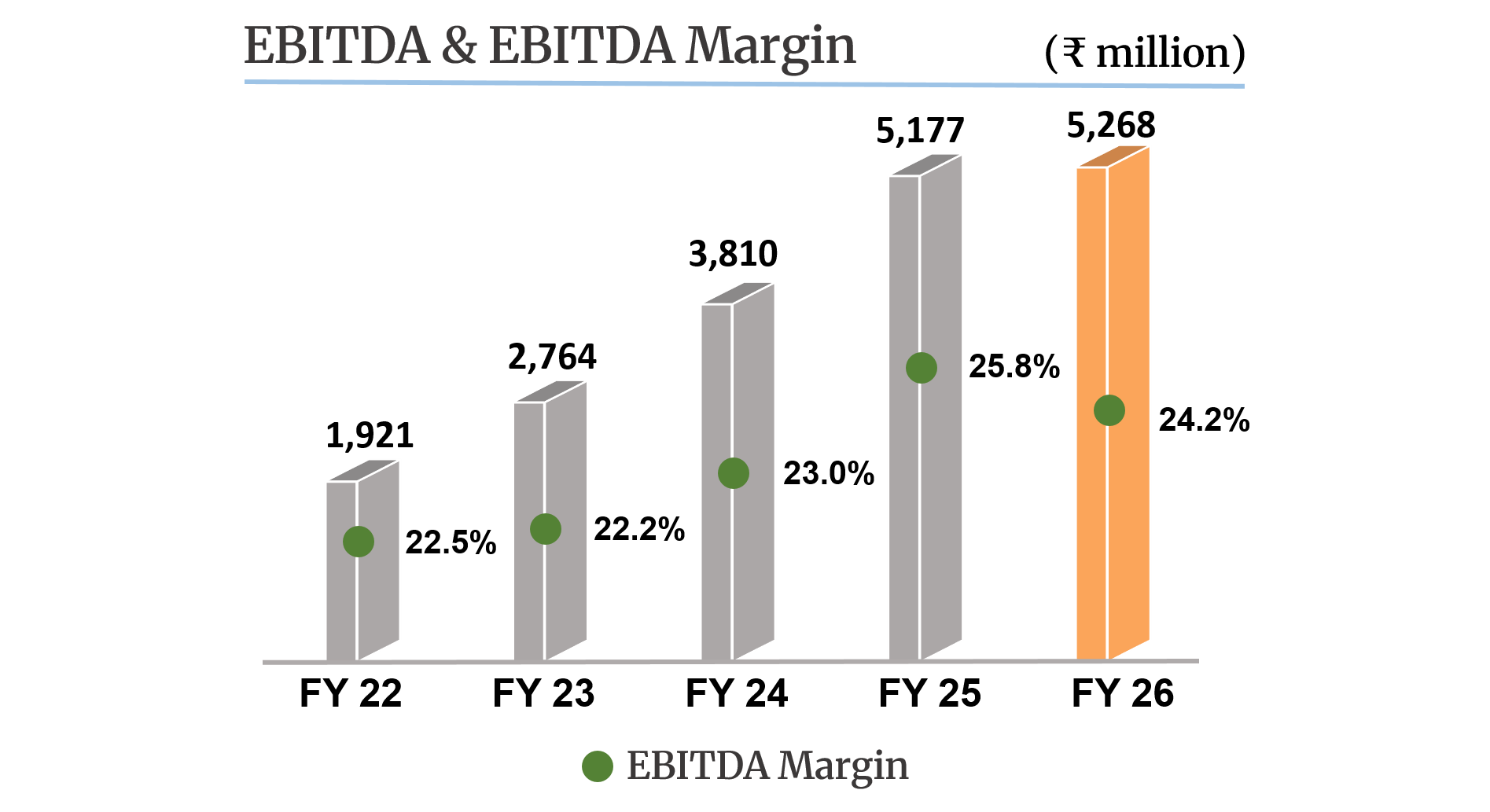

EBITDA

Profit Before Tax (PBT)

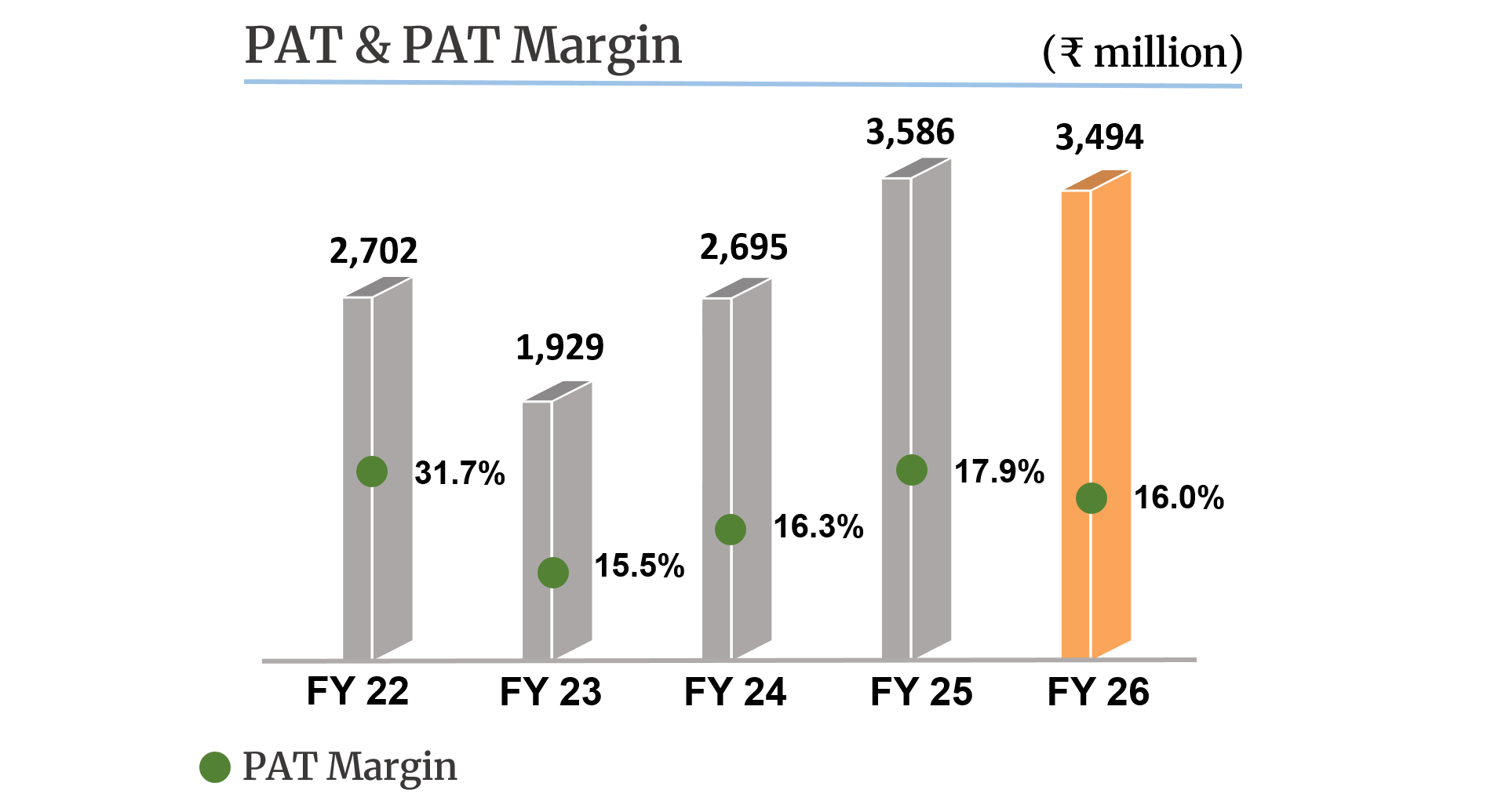

Profit After Tax (PAT)

*EPS (not annualized)

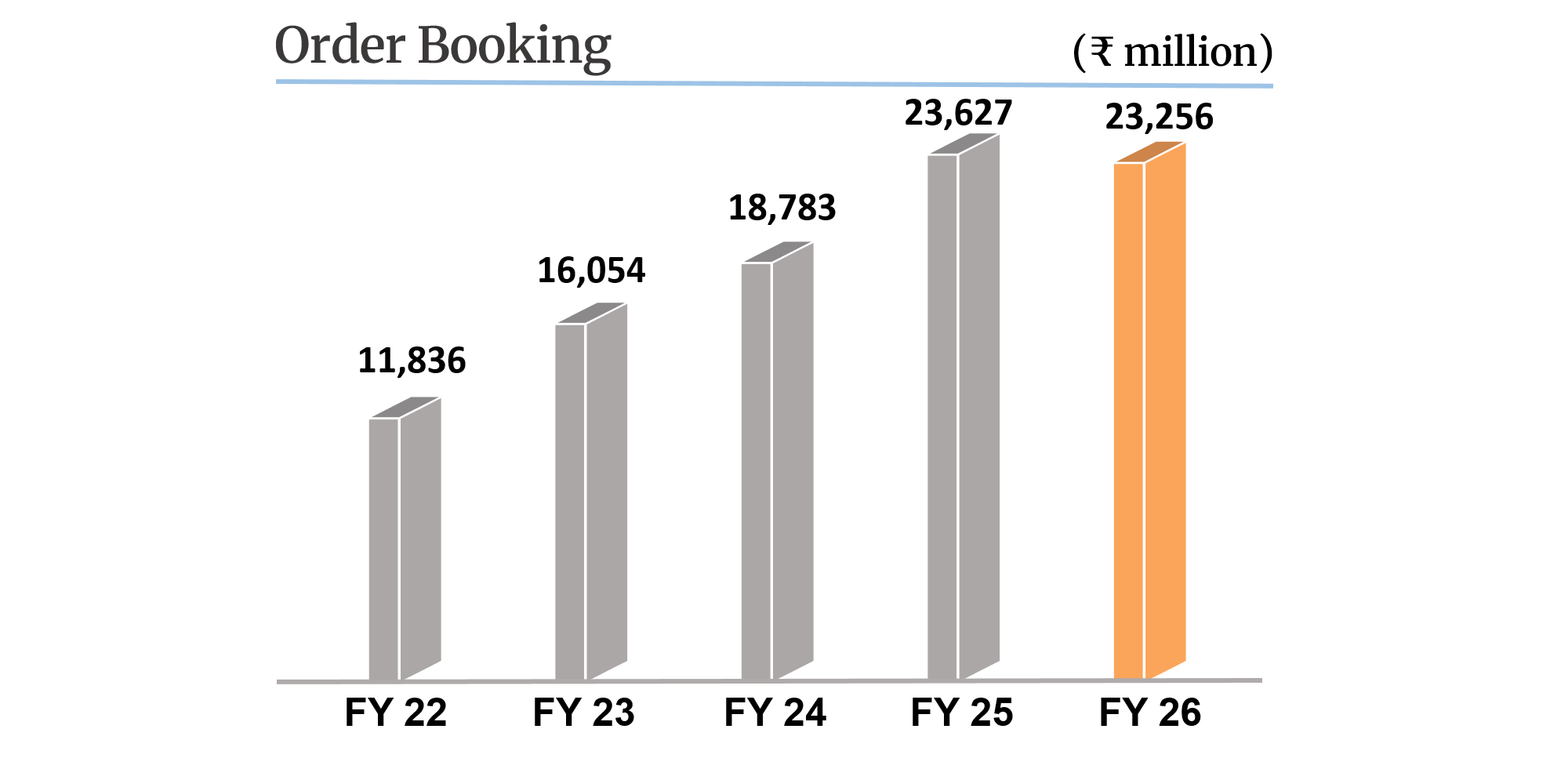

Outstanding order book

*Not annualised for the quarter

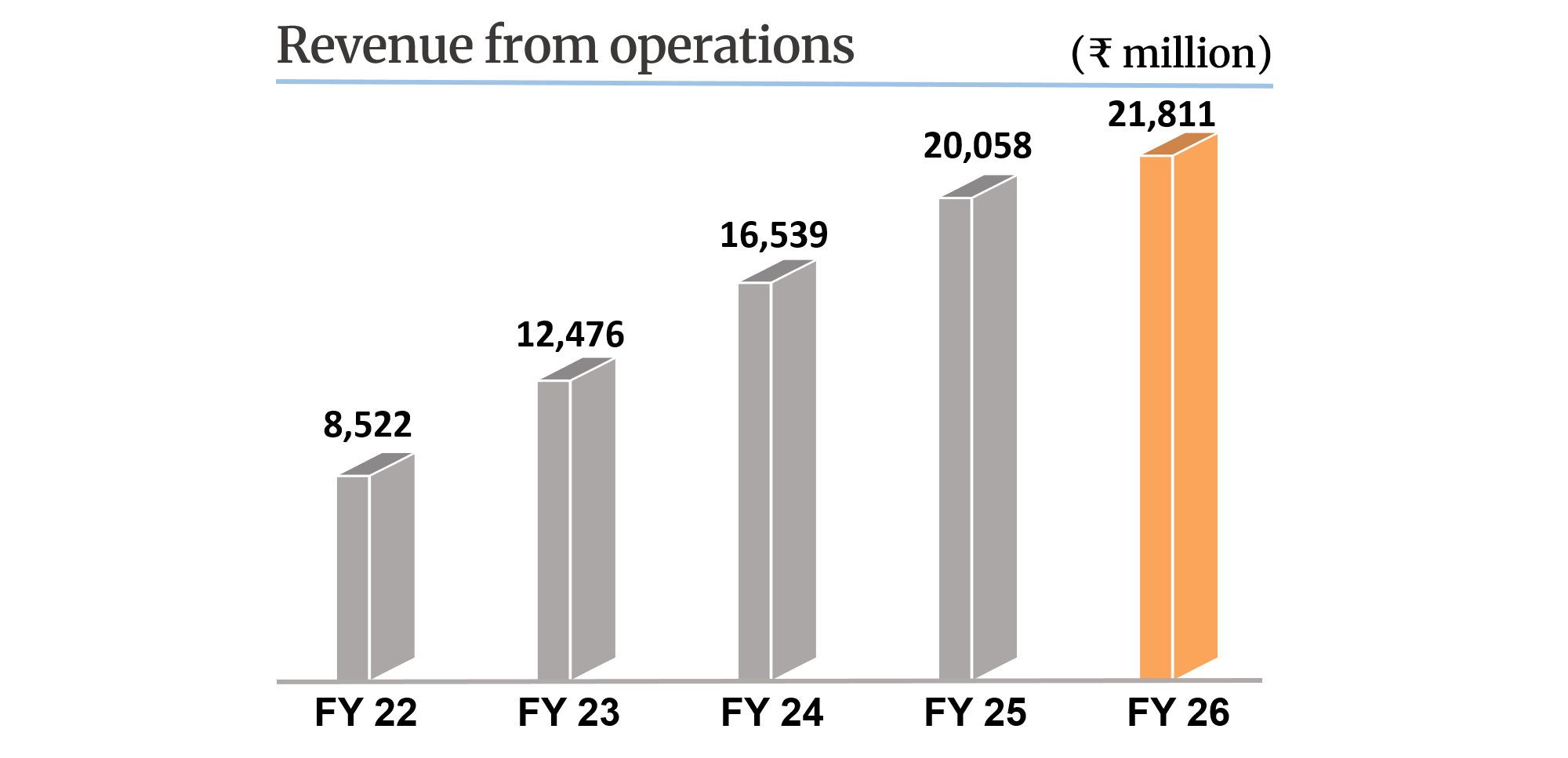

Revenue from Operations

EBITDA

Profit Before Tax (PBT)

Profit After Tax (PAT)

*EPS (not annualized)

Outstanding order book

*Not annualised for the quarter

Revenue from Operations

EBITDA

Profit Before Tax (PBT)

Profit After Tax (PAT)

*EPS (not annualized)

Outstanding order book

Revenue from Operations

EBITDA

Profit Before Tax (PBT)

Profit After Tax (PAT)

*EPS (not annualized)

Outstanding order book

*Not annualised for the quarter

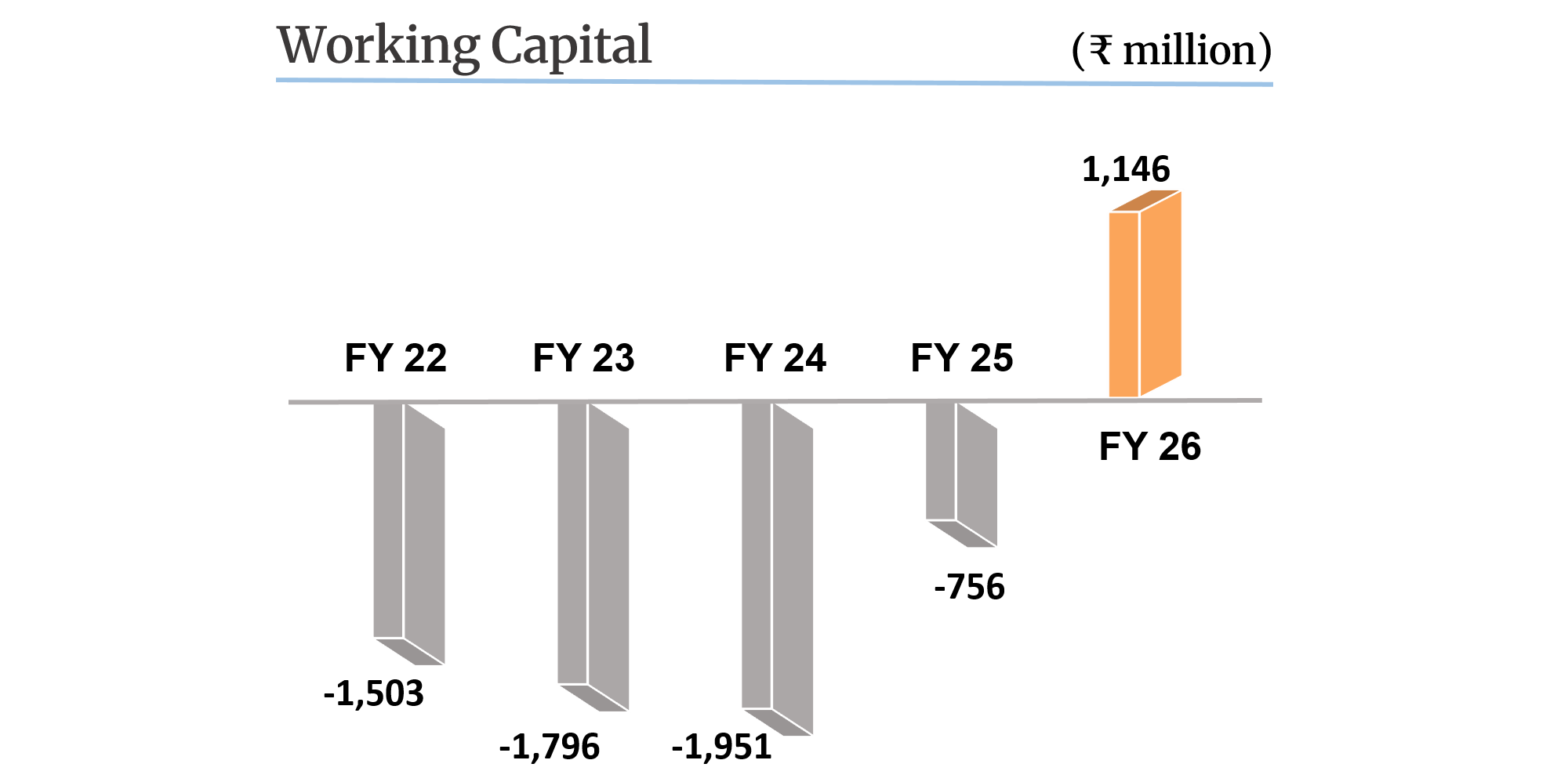

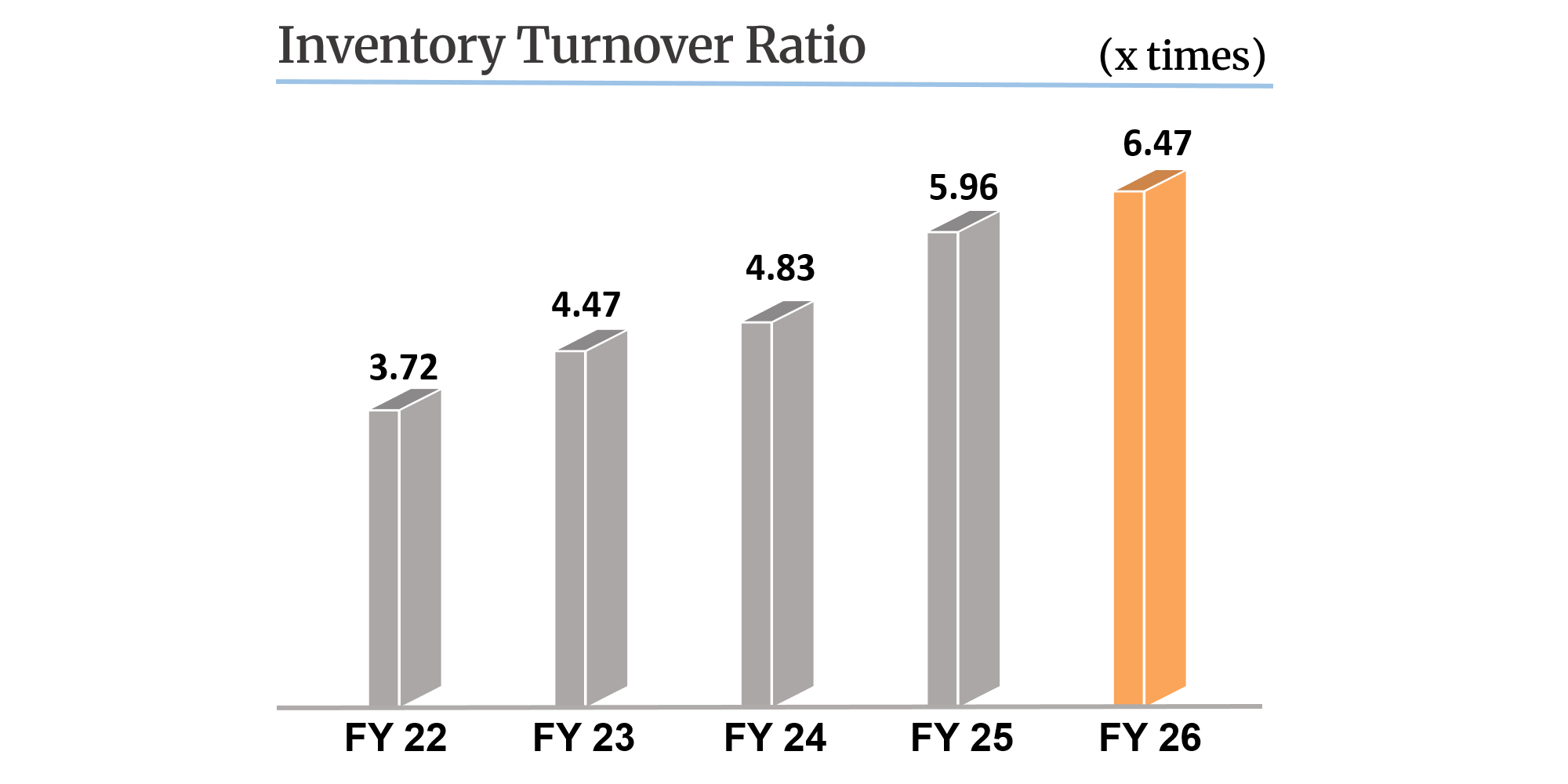

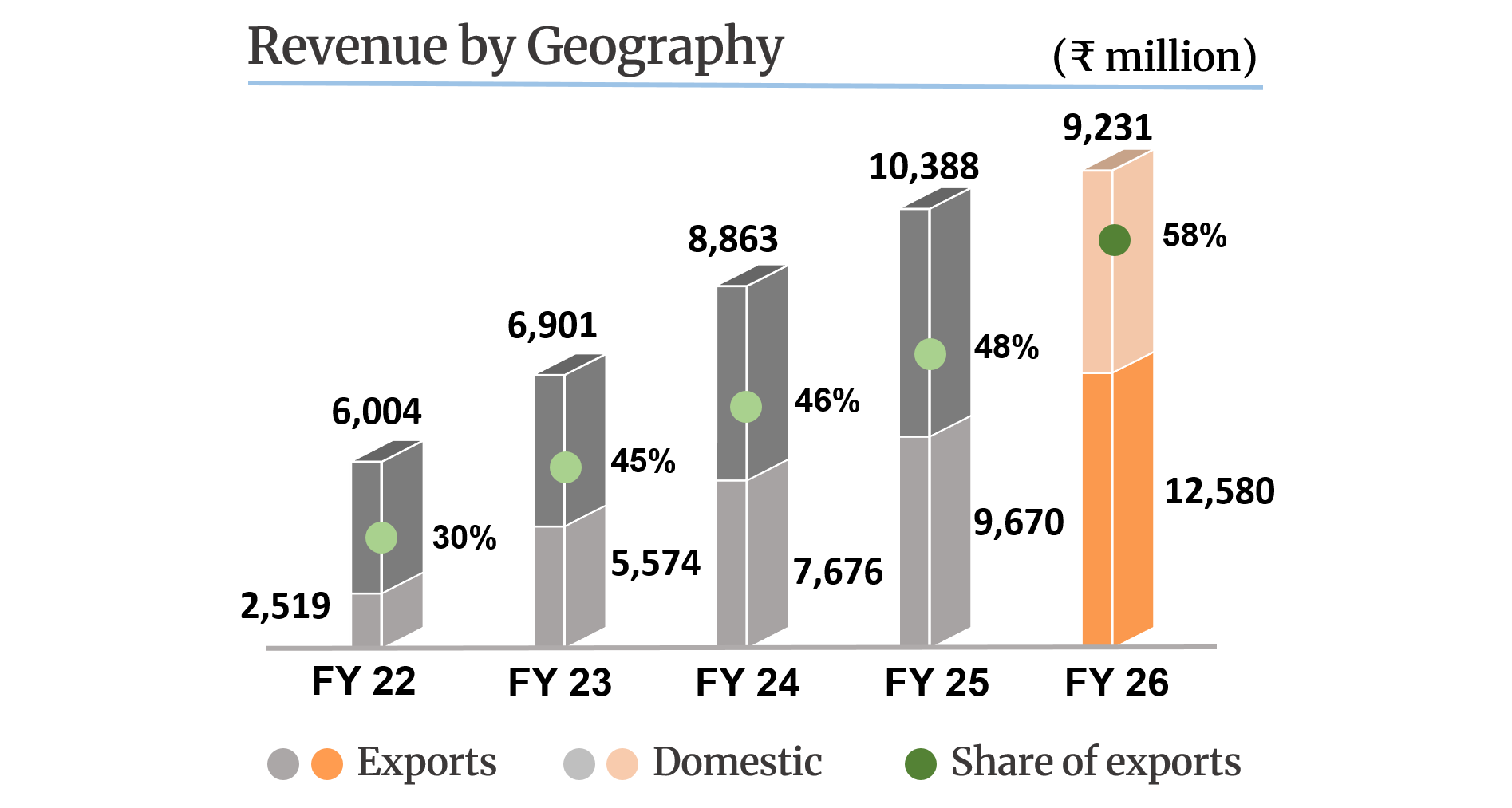

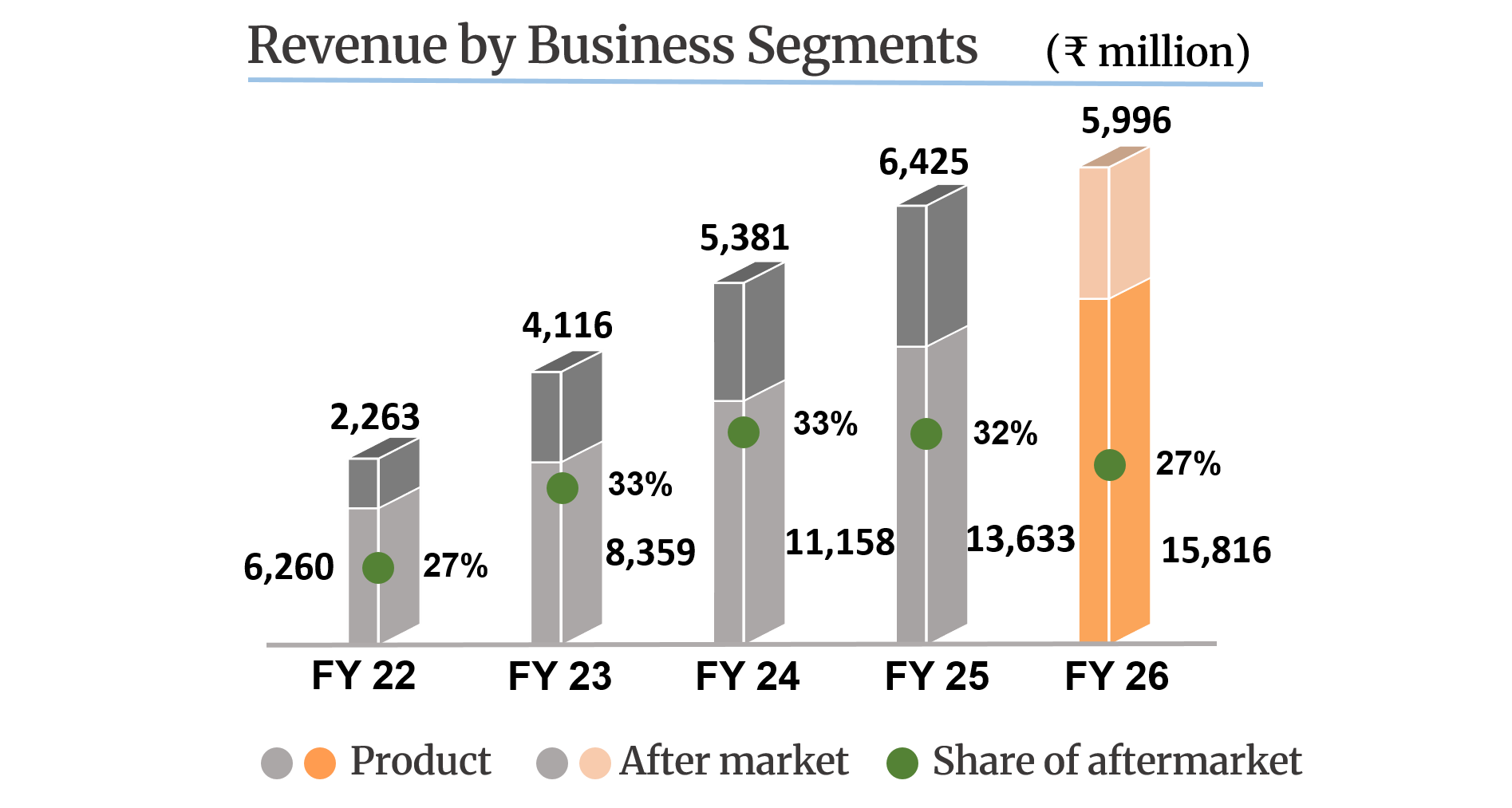

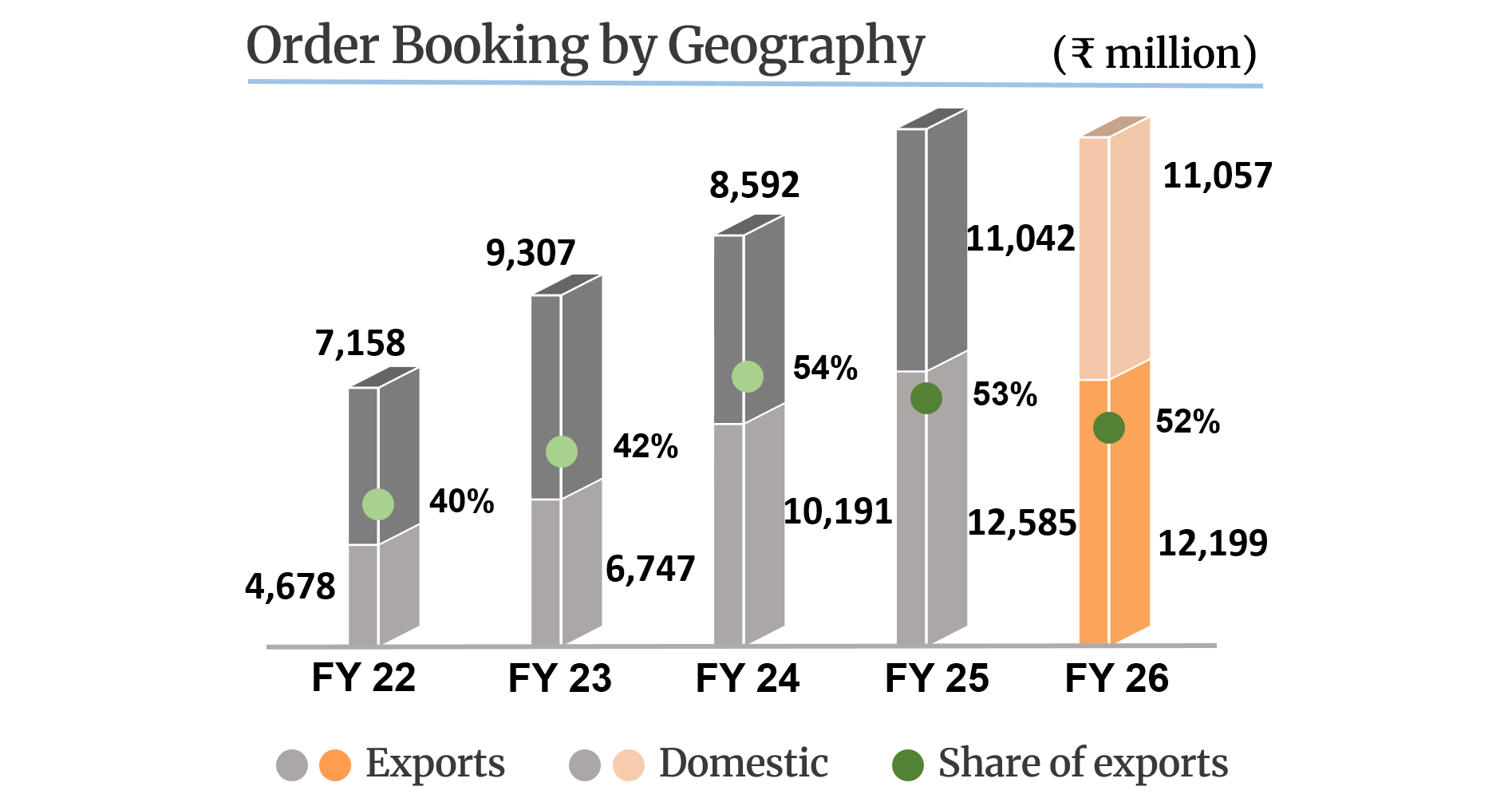

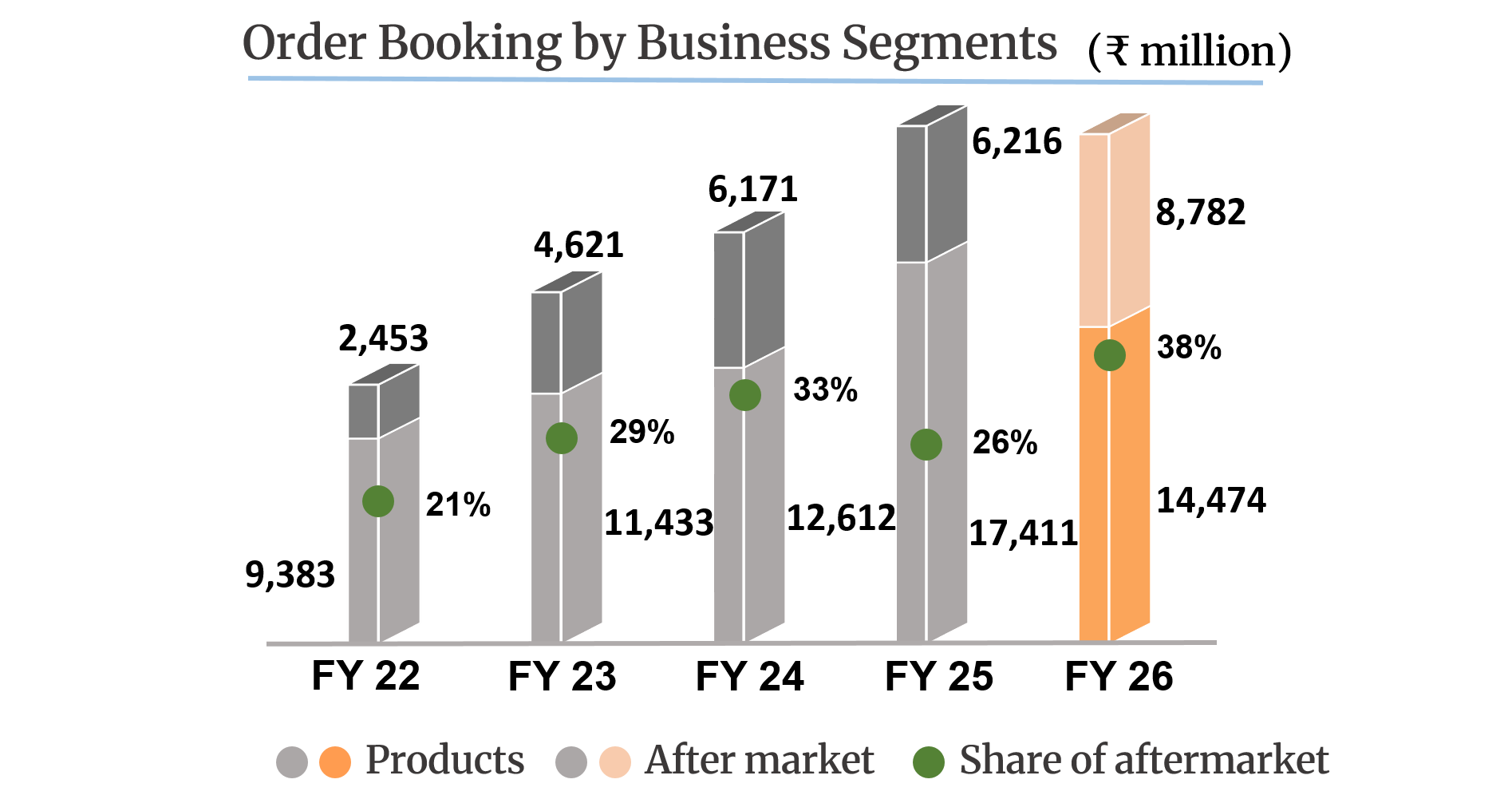

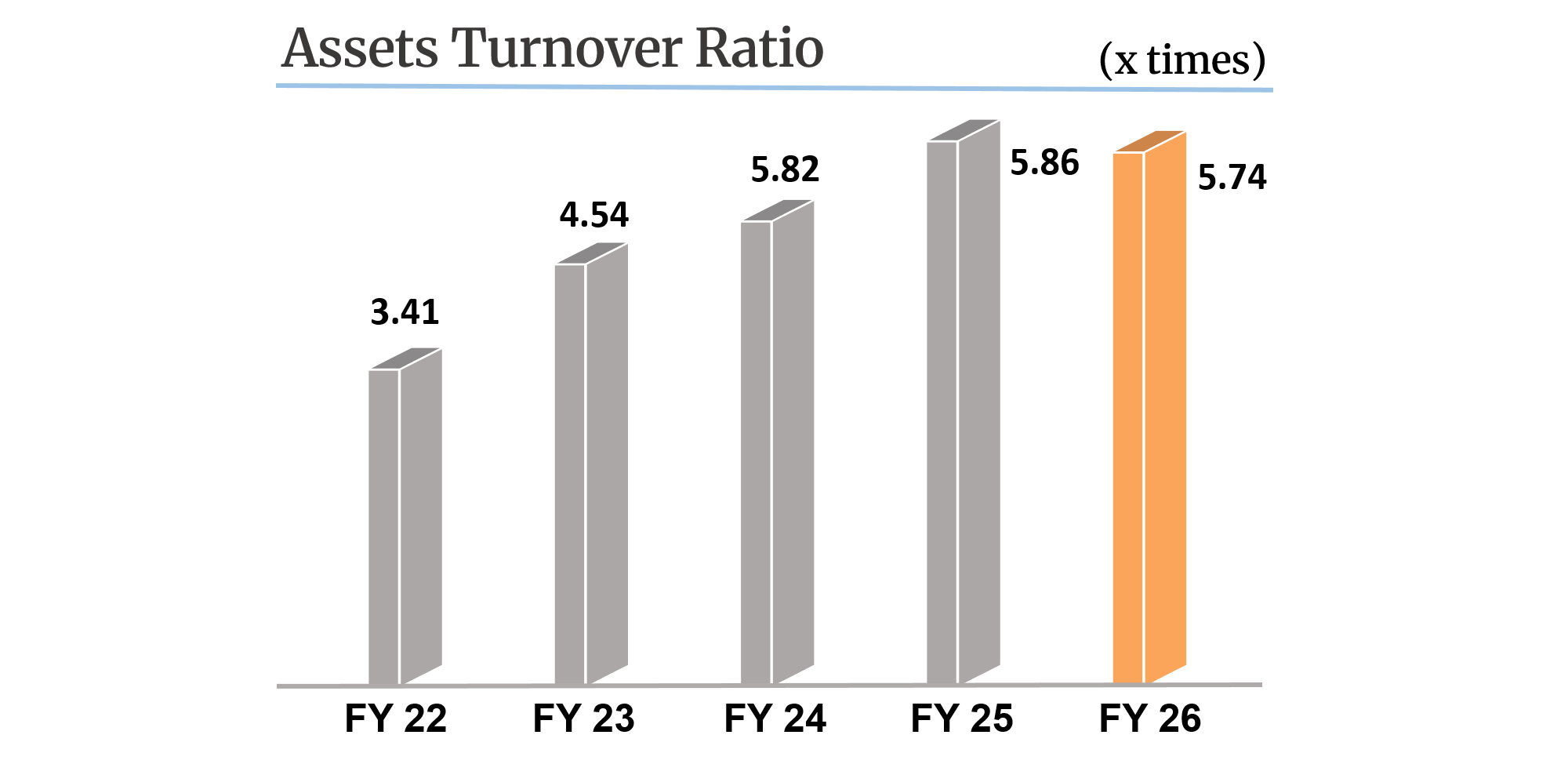

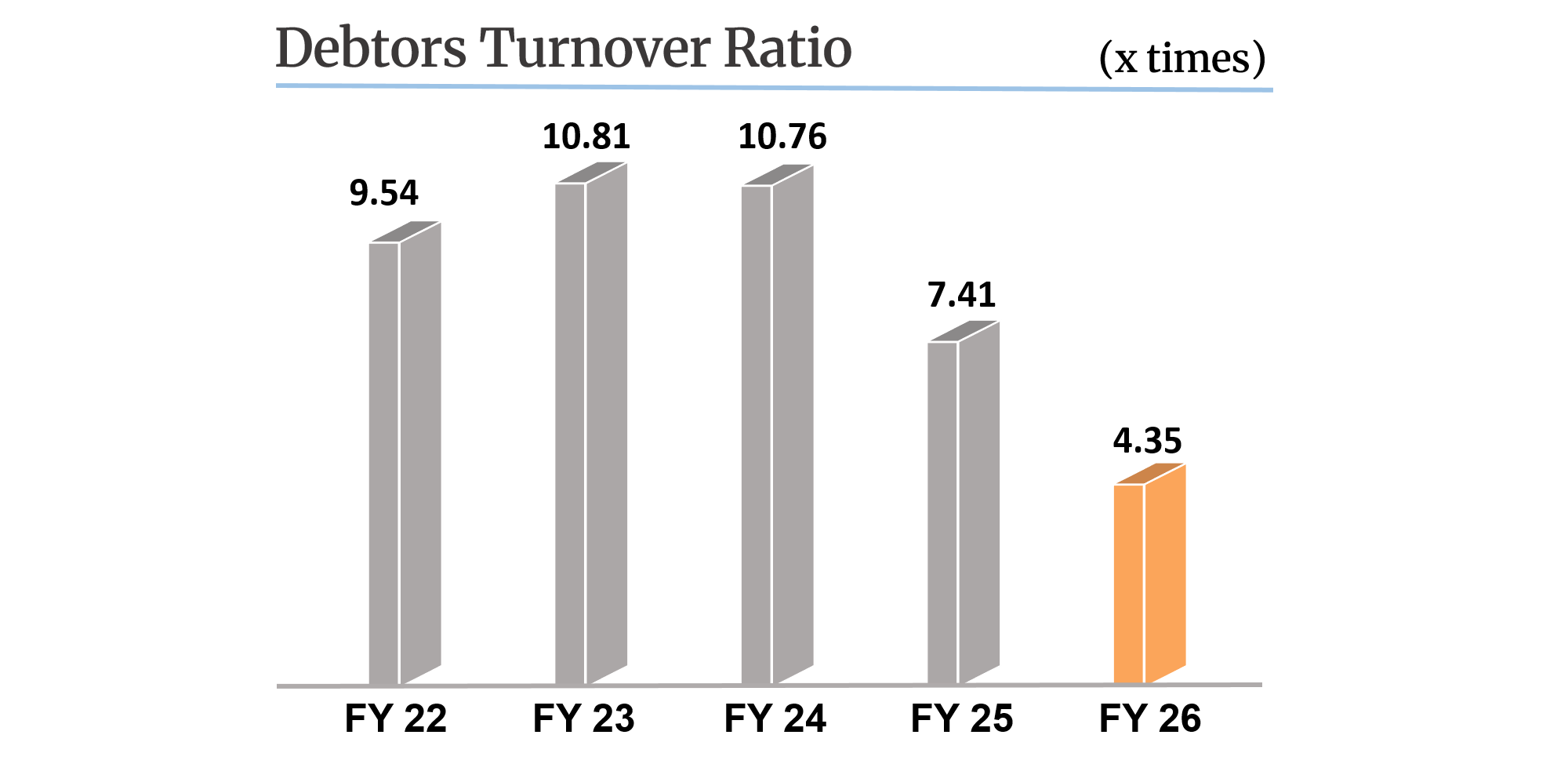

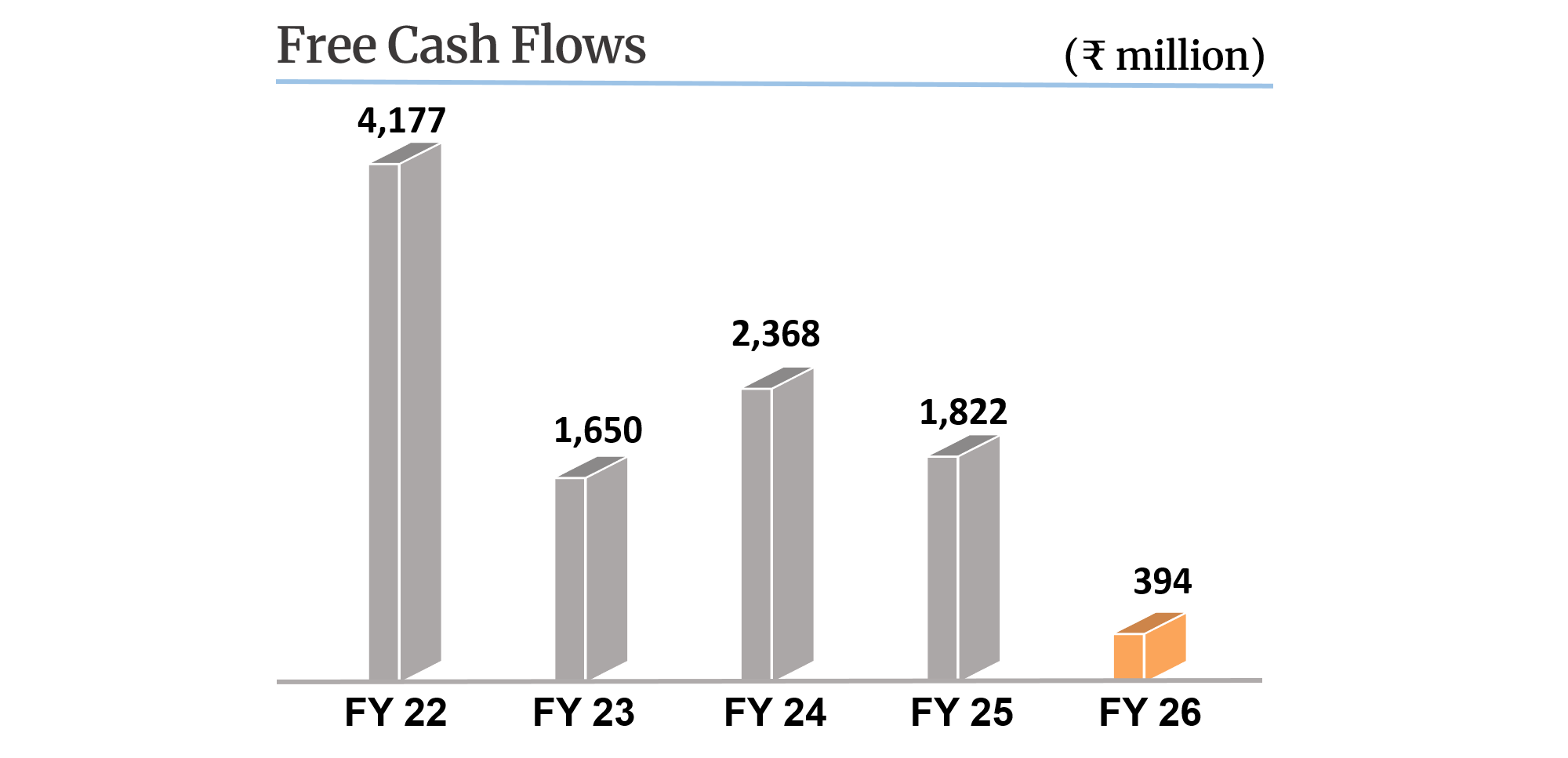

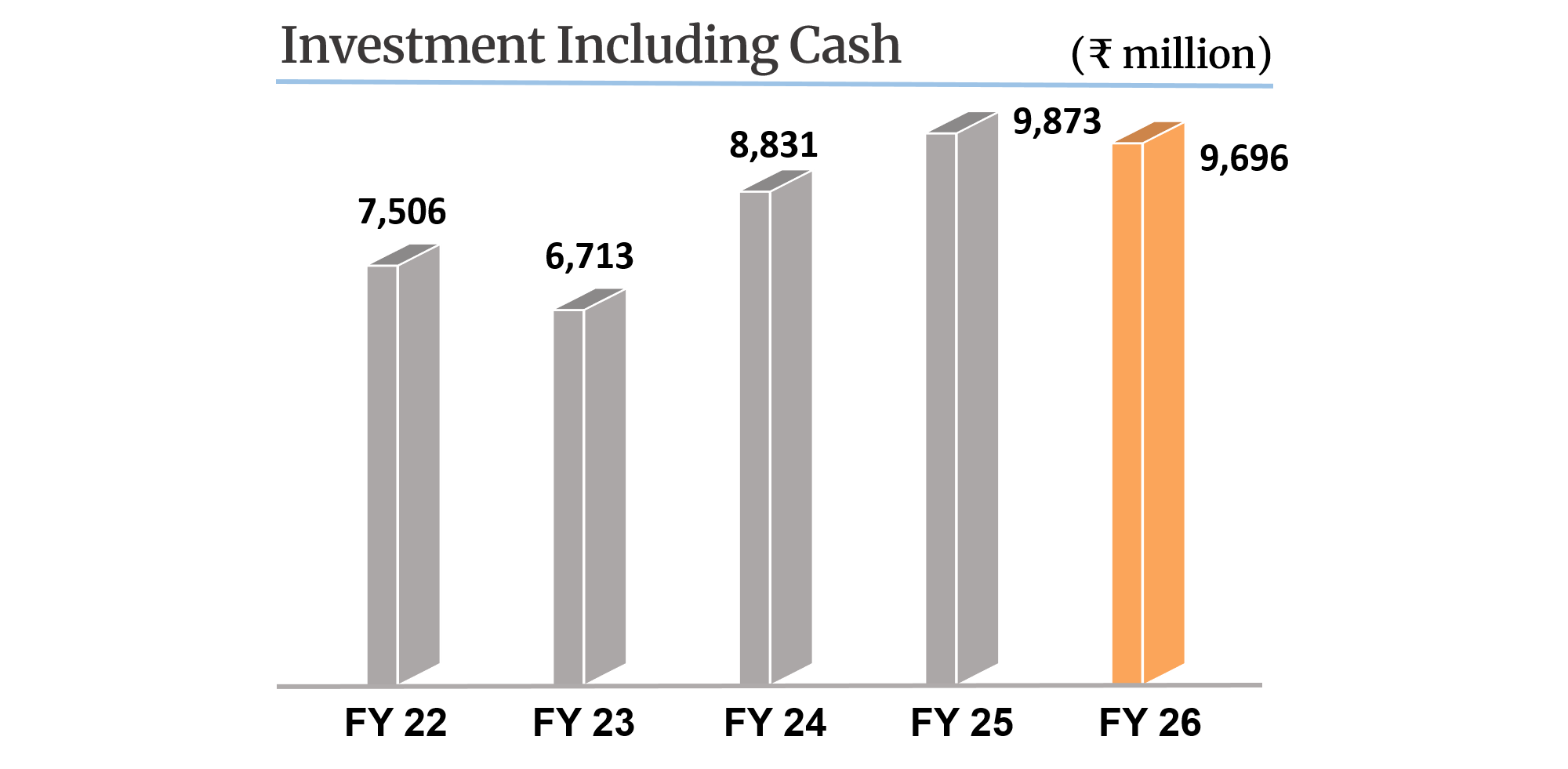

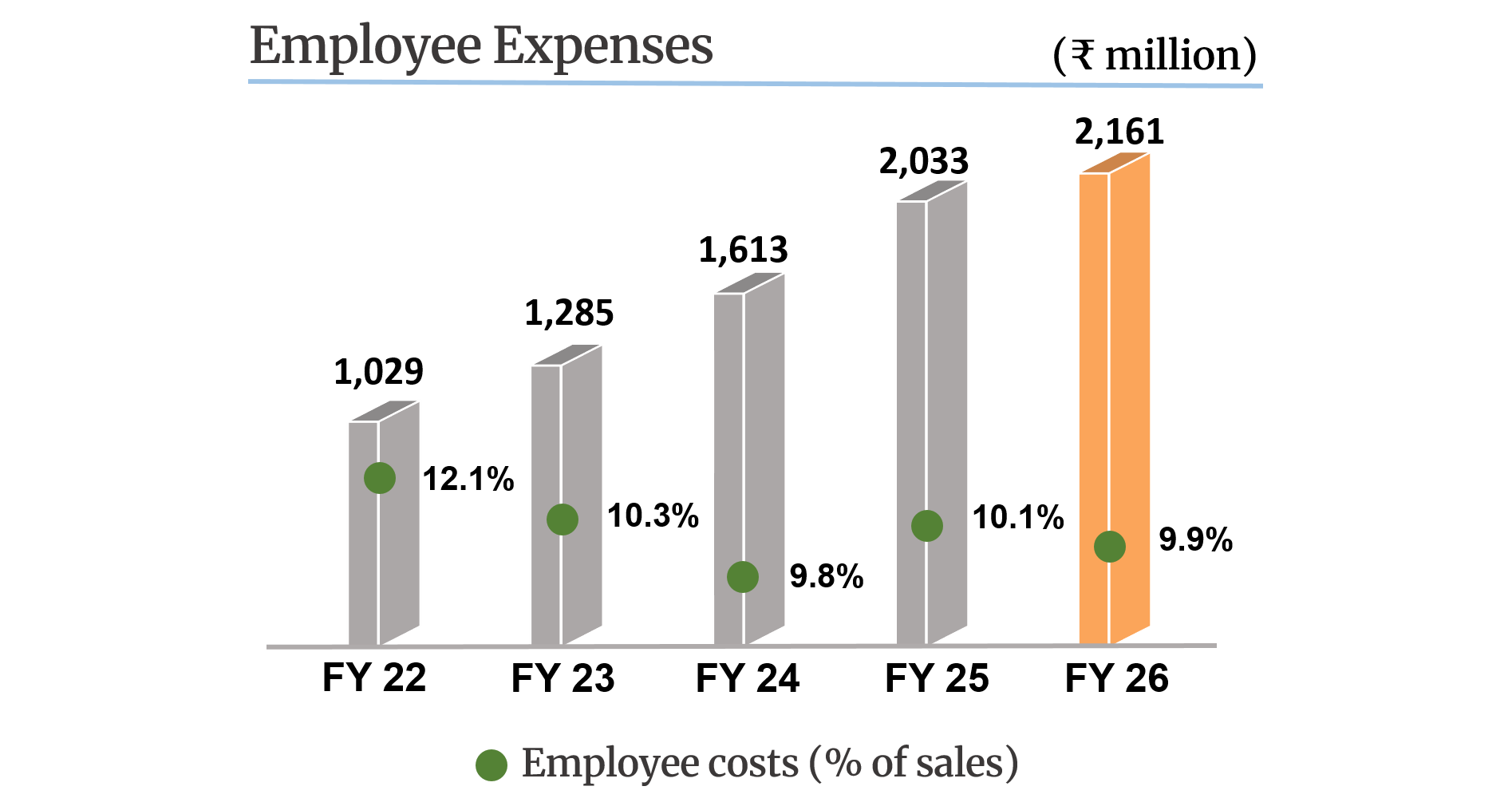

Key Performance

Highlights

Shareholder Services

For grievance redressal and queries related to shares, please contact:

Corporate Office of the Company

Mr. Pulkit Bhasin (Company Secretary)

Triveni Turbine Limited

Phone: +91-120-4308000

Fax: +91-120-4311010-11

Email:cs.compliance@triveniturbines.com

Registrar and Transfer Agent

Alankit Assignments Limited (Unit: Triveni Turbine Limited)

Phone: +91-11-4254-1234

Email:cs.compliance@triveniturbines.com

Website: www.alankit.com

Investor Relations Contact

For institutional investors’ / analysts’ queries, please contact:

Ms. Shreya Sharma

Head – Investor Relations & Value Creation

Triveni Turbine Limited

Phone: +91-120-4848000

Email: ir@triveniturbines.com